TradingAgents is an open-source Python framework that stages language models into role-specific agents — analysts, debating researchers, a trader, and risk-aware approvers- then routes their outputs through a graph so a final decision can be logged against a ticker and a date. The reference implementation lives on GitHub under TauricResearch/TradingAgents and ships with a CLI, Docker layout, and a programmatic entry point for experiments.

Why multi-agent layouts show up in finance code

One model answering “buy or sell?” in a single pass mixes evidence gathering, contrarian stress-testing, and risk appetite into the same context window. That is hard to audit and easy to overfit to whatever examples the model saw last.

Splitting the task into agents is less about magic and more about traceability: you can read which sub-report fed the trader node and which risk rule blocked an order. For background on generative systems in general, see what generative AI is; for industry-shaped use ideas (not trading picks), generative AI use cases by industry is a useful map.

If you are comparing visual agent builders to code-first graphs, Langflow for building agents is a different stack – TradingAgents is aimed at people comfortable editing Python config and API keys.

Roles inside TradingAgents

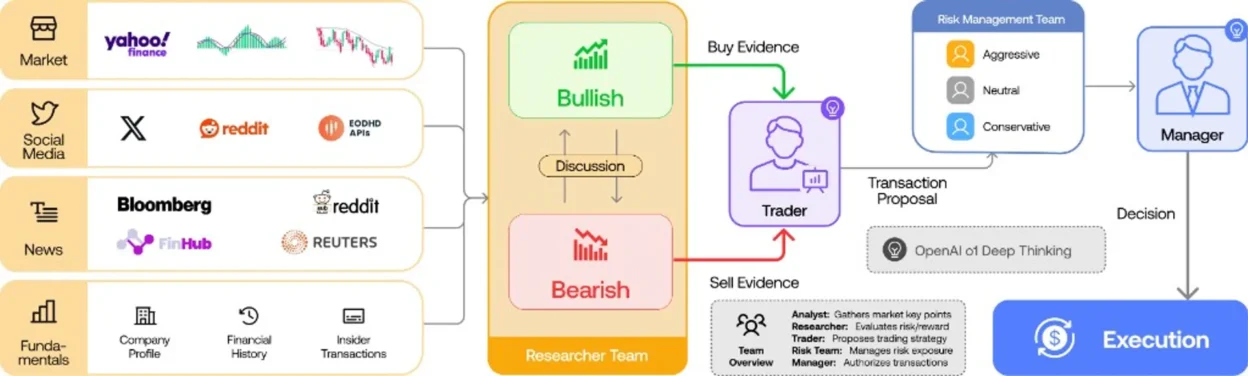

The public README describes a firm-shaped decomposition:

- Analyst team – fundamentals (financials and red flags), sentiment (social mood scoring), news (macro and headlines), technicals (indicators such as MACD and RSI in the docs).

- Researcher team – paired bullish and bearish roles that argue over the analyst packet so optimism and pessimism both get tokens.

- Trader agent – synthesises the thread into a concrete proposal (timing and size in the framework’s vocabulary).

- Risk management and portfolio manager — evaluates volatility, liquidity-style checks in the narrative, and approves or rejects before the README’s simulated exchange path records an execution.

That structure is the point: you are buying separation of concerns and replayable logs, not a single headline score.

Graph orchestration and model choice

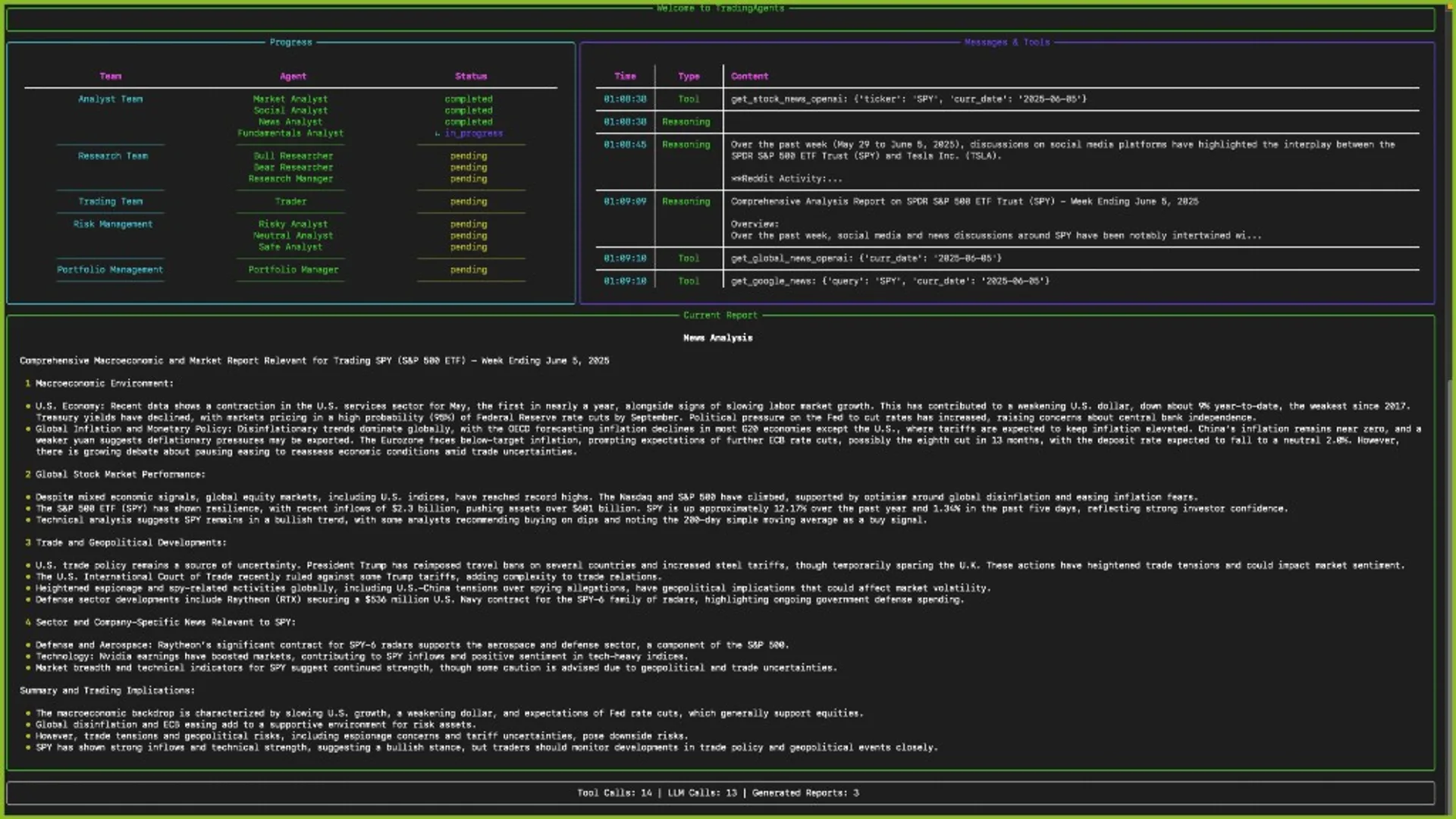

The authors state they built the workflow with LangGraph, which fits a state machine of nodes (agents) and conditional edges (debate rounds, approvals). Configuration is Python-side: you pick providers, “deep” vs “quick” model slots, debate depth, and similar knobs rather than hard-coding a single vendor.

Because model IDs and vendor SKUs change quarterly, treat the repository’s default_config and environment examples as the current matrix — wire the keys you actually own (commercial APIs or a local Ollama profile if you accept the ops cost).

How people actually run it

At a high level the project supports three entry styles common in modern Python repos:

- Install as a package from a clone (

pip install .in a fresh virtual environment is what the README illustrates). - CLI — an installed

tradingagentscommand orpython -m cli.mainfor an interactive picker (ticker, analysis date, provider, depth). - Docker Compose — copy the sample env file, drop in API keys, then run the compose service; an optional profile exists for Ollama-oriented setups.

Programmatically, the README’s TradingAgents package section shows constructing a graph object, calling propagate(ticker, date), and reading the returned decision structure — useful for batch backtests if you bring your own discipline about leakage, costs, and benchmark honesty.

Limits, ethics, and the disclaimer that matters

The README is explicit: the framework is for research. Outcomes swing with model choice, temperature, calendar period, data gaps, and plain hallucination risk. Nothing in an open GitHub repo replaces compliance, exchange rules, or fiduciary duty.

Practical takeaway: use TradingAgents to prototype research workflows and teach multi-agent design not as a black box that justifies size in a live account. If an output looks too clean, assume it is wrong until cross-checked against primary filings and your own risk limits.

Frequently asked questions

Is this legal financial advice?

No. It is open-source software and an academic-style framework. Anything that touches real money needs licensed professionals, disclosures, and jurisdiction-specific rules the repo does not implement.

Does it place real trades?

The documentation describes a simulated execution path after portfolio approval. Wiring a live broker would be your own integration and compliance burden.

Do I need paid LLM APIs?

The project lists multiple commercial providers and a local Ollama-style path. Paid APIs buy latency and capability; local models buy privacy at the cost of ops and often weaker tool use — pick based on your experiment budget, not hype.

Where should a beginner start reading?

Read the README end-to-end, then the TradingAgents package block for the import pattern, then default_config and the env examples. Run the CLI once on a toy ticker before you edit graph code — you will learn faster with logs than with a blank main.py.

Treat every agent output as a draft memo: sign it with your own data, your own risk function, and your own “no trade” default.